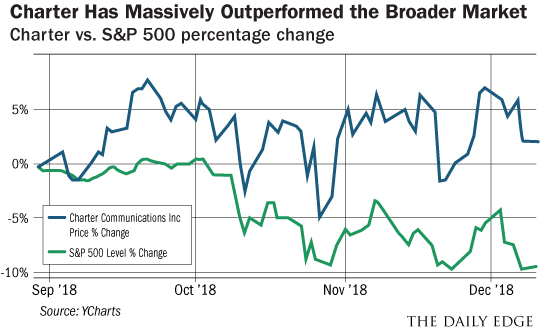

This post Beat a Legendary Hedge Fund Manager at His Own Game! appeared first on Daily Reckoning. No cord, no problem. At the end of August, I noted that the stock market had served us up an opportunity to purchase shares of giant cable and broadband provider Charter Communications (CHTR) at a very attractive price. The reason that Charter shares were on sale is that the market was greatly misinterpreting how big of a problem "cord-cutting" was for the giant cable company. So far so good with my August trade idea. Charter shares have outperformed the S&P 500 by almost 12 percent in the subsequent three and a half months.

As I noted back in August though, I believe there is a lot more to come. With Charter's low valuation and relentless share purchase program, the company could generate 20 percent annualized cash flow per share growth over the next three years ? and ultimately double in share price. Today, I'm going to show you another company in this sector that the market is similarly undervaluing? Here's What the Market is Missing?The market isn't wrong about the fact that cable customers are choosing to "cut the cord" at a rapid pace. In fact, the rate at which people are leaving traditional cable is accelerating ? having tripled in the past five years.1 Viewers are increasingly opting for the wide world of streaming entertainment that is available from providers like Amazon, Netflix, Hulu, YouTube, Sling TV and others. What the market is very wrong about, however, is how this is going to impact the cable companies. The market needs to understand that a customer who cuts the cord on cable isn't the same as a customer who is ending their relationship with the cable provider altogether. This is key, because the cable provider is most often the same company that is supplying them with broadband service. Further, once that customer cuts the cord to move exclusively to streaming entertainment, what usually happens is that they decide to get a faster connection. The customer does that so that they can stream video across multiple devices and actually enjoy it without lags. That faster broadband connection is more expensive ? which means more revenue for the broadband provider. If you have ever tried to watch a streaming video that is constantly pausing, you know that not upgrading to a faster connection is simply not an option. The repeated starts and stops of watching a constantly pausing/freezing video is torture! You will pay anything to make it stop! So not only does the cable company generally retain the cord-cutting customer as a broadband customer, the company does so while selling the customer a much higher margin product. The margins on cable are thin. That is because the cable company has to pay for the content being provided which in recent years has become incredibly expensive. Have you ever checked out the deals that some television and movie stars are getting? Meanwhile, the margins for selling broadband space are fat. Very fat. According to the chief financial officer of Cable One, residential high-speed data and business services have four to five times the profit margin of video.2 That makes cord-cutting sound more like a blessing than a curse. A Hedge Fund Legend Agrees with My Cord-Cutting Trade ? Just Likes a Different StockHedge fund legend David Einhorn of Greenlight Capital agrees with this cord-cutting overreaction investment thesis. It turns out that while I was writing about Charter Communications in August, Einhorn was busily buying shares of another undervalued cable and broadband provider. Einhorn's preferred way to play the cord-cutting overreaction is through Altice USA (ATUS). But rather than have me put words in Einhorn's mouth, here is what he had to say about purchasing Altice in Greenlight Capital's third quarter investor letter: "The Partnerships made a new investment in Altice USA (ATUS) at an average price of $18.38. ATUS trades at an EBITDA multiple discount to pure-play cable peers despite better free cash flow conversion and better new investment opportunities. ATUS is rebuilding a majority of its network with fiber in the coming years, with an anticipated 40-50% return on its investment. The shares trade at a 10% cash flow yield, in part because of market concerns over cord-cutting. But when a customer drops linear video and instead streams video through their broadband connection, data consumption rises very dramatically, which is positive for ATUS."

As I write this, shares of Altice USA actually trade for a slightly lower price than the $18.38 average price that Einhorn paid in the third quarter. So not only do we get to piggyback the research he spent time and money on, but we also get to buy shares at a better price. I like the sound of that! Here's to looking through the windshield,

Jody Chudley

Financial Analyst, The Daily Edge

EdgeFeedback@AgoraFinancial.com5 1 The number of cord-cutters has tripled in the last 5 years, and it's starting to hurt the TV channels

2 Cable One Claims Highest Margin in the Cable Industry The post Beat a Legendary Hedge Fund Manager at His Own Game! appeared first on Daily Reckoning.  |