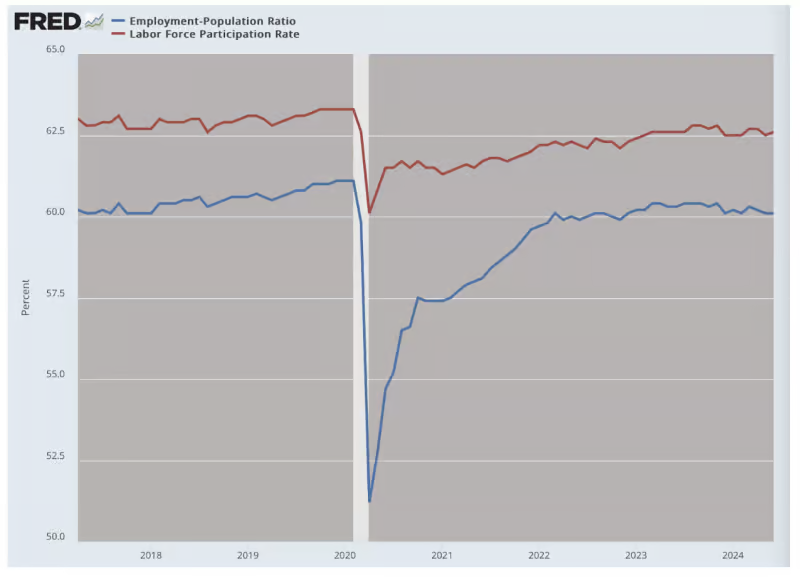

This post 10 Lingering Hangovers From Lockdowns appeared first on Daily Reckoning. The sudden economic lockdown of March 2020, the world over, was one of the more shocking moments in history. It was initially advertised to be two weeks. But as time went on and the lockdown period was extended longer and longer, it became clear that the whole point was to wait for a vaccine. This was based on the evidence-free supposition that the whole population was under threat and that the shot would fix the problem. The world economy crashed ? entirely by intention and by force ? as never before seen in modern times. We've seemingly ?recovered.? But in reality, we're still living with the aftereffects of lockdowns. Below are 10 lingering economic hangovers we're still suffering from. Read on. Post-Lockdown Economics (Continued)By Jeffrey Tucker 1. The labor markets have never recovered. Both labor participation and employment/population ratios remain below what they were in 2019. Maybe this is the result of retirement. Maybe it's disability. Maybe it is just demoralization. Regardless, we never got back to normal. All the talk of the great job machine since 2021 is nothing but people finding work again after having been displaced during lockdowns or new people coming into the market.

The job market has not been ?hot? by any standard. Monthly data reports institutional surveys, which double-, but rarely household surveys which show continuing weakness. The divergence between the two has never been higher. We're nowhere near a pre-lockdown trend.

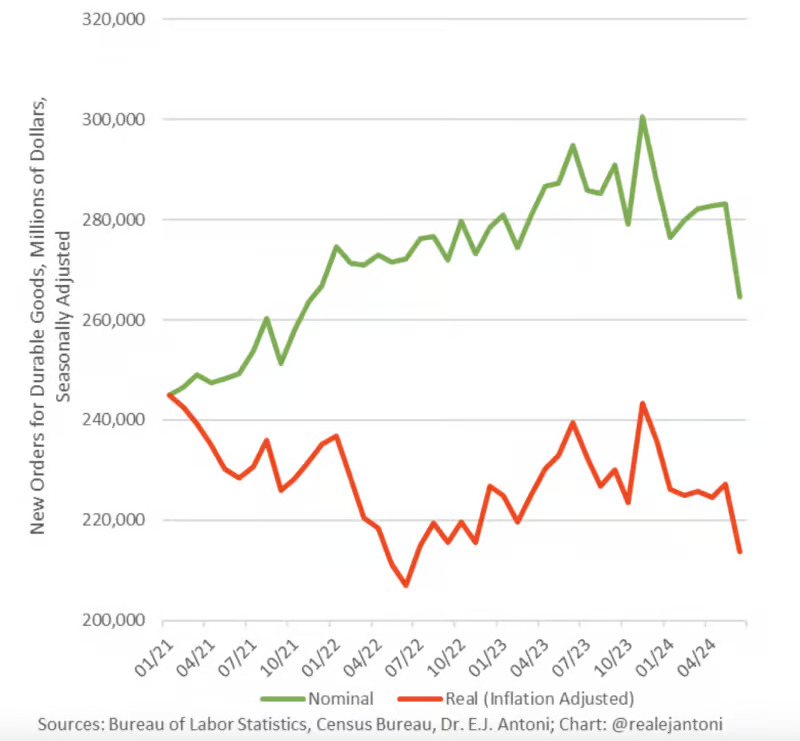

2. Stimulus was wiped out by inflation. When the checks started arriving directly in bank accounts, people were doing absolutely nothing at home and business was getting revenue from government even when their doors were closed, it seemed like some Nirvana had dawned. Riches were flowing from heaven. That lasted about 18 months. Once inflation came along, the purchasing power of those dollars was zapped away. Money creation had been on a level never before seen in modern times; some $6 trillion was created out of thin air to buy stunning amounts of debt. It was all taxed away in the most ancient scheme of tricking the public. 3. Retail sales and wholesale factory orders are not up. Among all the usual data releases, only the GDP numbers are routinely adjusted for inflation. For most reports, you have to do that independently. Retail sales and factory orders are reported in nominal terms, which works fine in normal times but in inflationary times, this habit produces absurdities. It ends up clocking more spending on the same goods and services simply because everything is more expensive. E.J. Antoni has been all over this point. Even adjusting usually severely underreported inflation shows that neither retail nor wholesale has genuinely risen. Again, these adjustments are based on conventional CPI data so the actual reality is much worse.

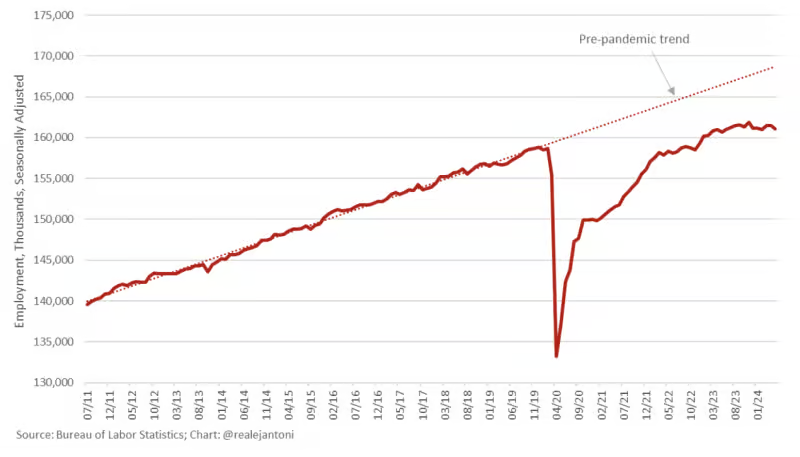

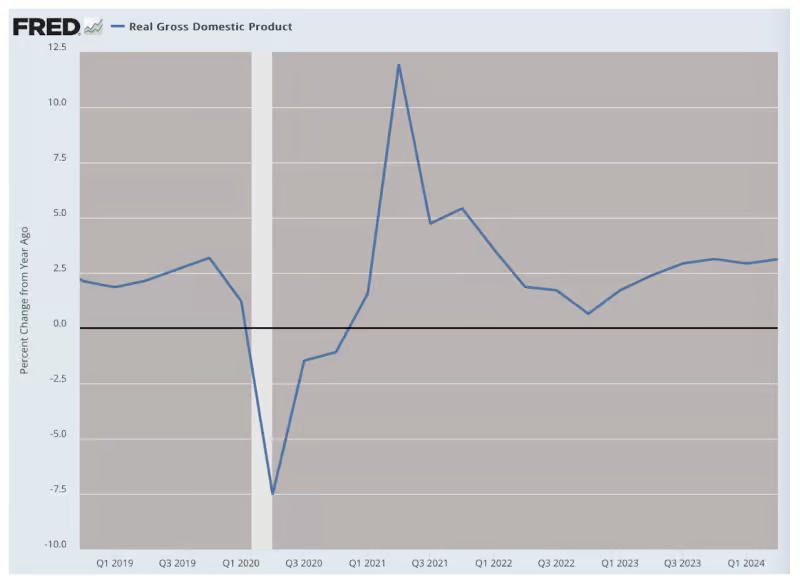

4. Output has not increased. In the conventional telling, the lockdowns created an instant recession but it only lasted a couple of months. Once the stimulus was released and the economy opened up a bit, the boom reversed all the damage. We've been growing moderately ever since.

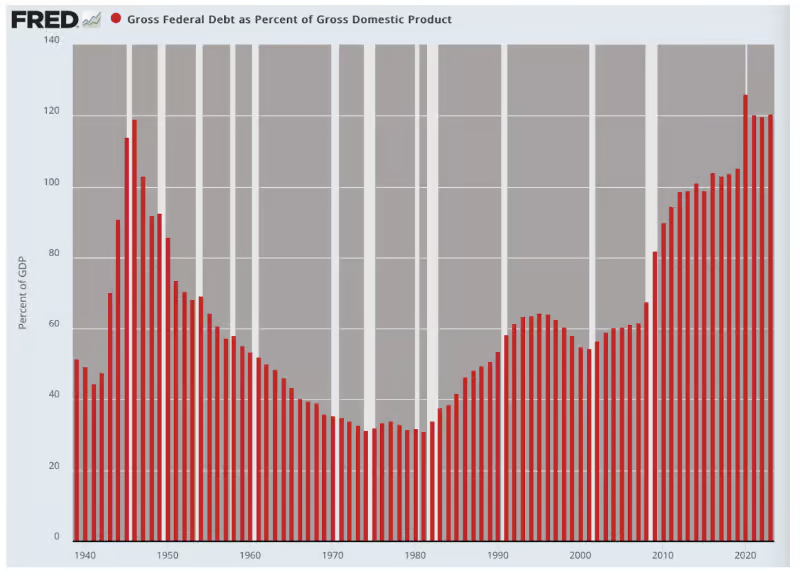

In other words, the conventional data tells the story of the most implausible scenario, a beautiful lockdown that did no net damage but merely paused economic life until everything went back to normal. But what if this is completely wrong? How could it be? There are two major factors: the inclusion of government spending as constituting economic growth and an inflation adjustment that is lower even than the CPI, one crafted especially for use in national income statistics. Everyone knows today that the statistical prosperity of wartime in World War II was not real due to the inclusion of government as the main contributor to supposed economic output. Government debt as a percentage of GDP has reached and surpassed wartime levels in the last four years. This should tell us something important about the credibility of this seeming recovery.

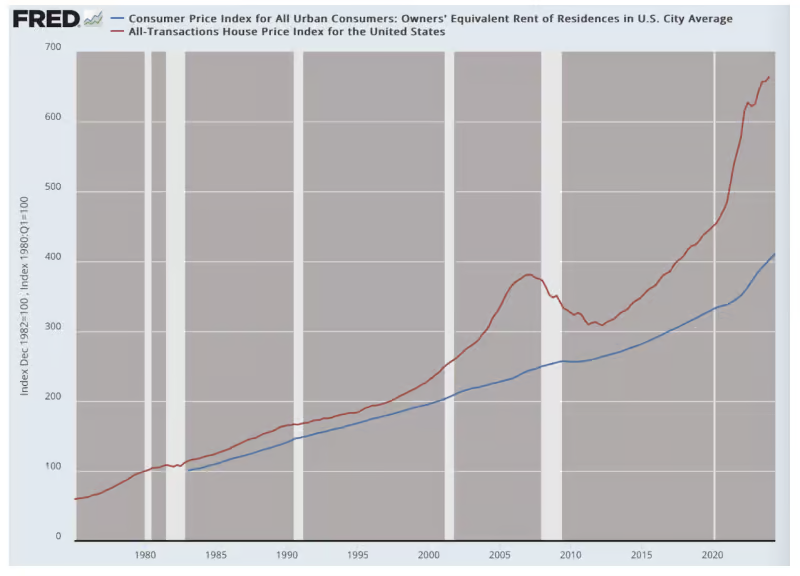

5. The inflation data is fake. According to the official data, the dollar of January 2020 has sustained 82% of its value, which is to say it has lost only 18 percent of value over four years. Think about this in your own life, based on your bills, your shopping and what you can see with your own eyes. Think back to the good old days of 2019. In what world is it even vaguely plausible that the prices you pay (or consider paying but then decline to pay) have gone up only 18%? How is the CPI able to render price increases this low? Because the data excludes interest rates, homeowners insurance, taxes, shrinkflation and added fees. Data on health insurance prices are adjusted downward for medical consumption. The data on home prices is fed through a wildly complicated formula called homeowners equivalent rent. It has become a fantasy. In the chart below, the red line is excluded from CPI in favor of the blue line.

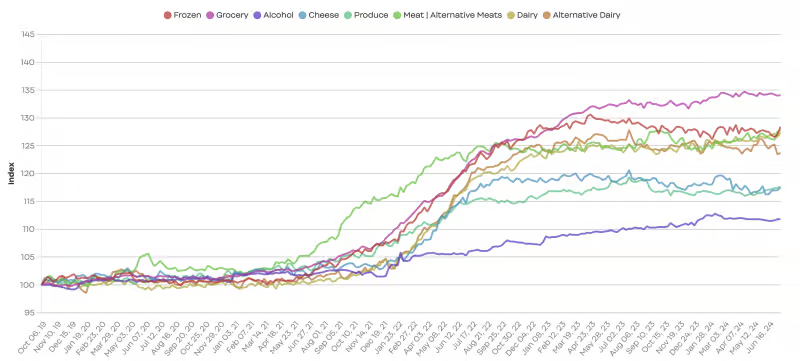

Even on specifics, the Bureau of Labor Statistics can't seem to reflect actual industry prices. The BLS has food prices up 26% since 2019. But industry data has grocery up 35 per. The least price increases are in retail liquor (11%), which is precisely why cocktails, wine and beer are up so much at restaurants: it's a good place to extract profit margins.

Then you have the black box of hedonic adjustments, which allow bureaucrats to re-render the price of any product with changed quality with some perception that, after all, you don't mind paying more for higher quality, so therefore it is not really increasing in price. Finally, you have the effective exclusion of most main forms of shrinkflation and added fees. How much does all this add to the CPI? We don't really know. It's not wildly impossible that real inflation over four years has been 30% or 50% or higher. Adjust all the other data for that and you gain a completely different picture of what is happening. 6. Trade blocs have formed and will not save us. When all supply chains in the world froze in March 2020, and then gradually reopened based on national politics, we saw the fraying of 70 years of global integration. The chip manufacturers moved from supply for cars and other industrial goods in the U.S. to laptops and gaming machines in the Asian sphere of influence. Soon after the opening, the U.S. de-dollarized Russian assets, giving BRICS new incentive and energy to become more robust. For years later, the new shape of the world is becoming apparent: It's all about spheres of political influence, thus shattering a driving force of global economic growth for many decades. 7. Property rights are not secure. Never before in U.S. history have so many small businesses been shut down coast to coast with such brutality. When they opened again, it was often only at throttled capacity, giving a huge boost to big over small restaurants and hotels. This was all a foundational attack on property rights, the very core of a functioning economic life. This surely shook the psychology of business formation nationwide. Though we have no empirical data on this, it is still the case that a state that attacks property this way cannot expect a thriving world of business startups. If your business can be shut down for such strange reasons, why start one at all? This is the sort of institutional problem that causes economic decay in imperceptible ways. 8. The debt is out of control; personal, corporate and government. Plenty of people have written about the problem of the government debt, the interest on which three-quarters of taxes are now directed to pay. The ship of corporate debt sailed long ago with the wild experiment in zero interest rates by the Federal Reserve after 2008. Rates were reversed to deal with inflation. The resulting high rates are deeply painful for any non-public business that depends on leverage for its operations: The consumer debt problem is more striking still: In times of high interest, savings should be going up, not down, and debt should be going down, not up. The opposite is happening simply because real income is falling dramatically and has been for three years. Even using conventional CPI data, we have not yet recovered from the lockdowns.

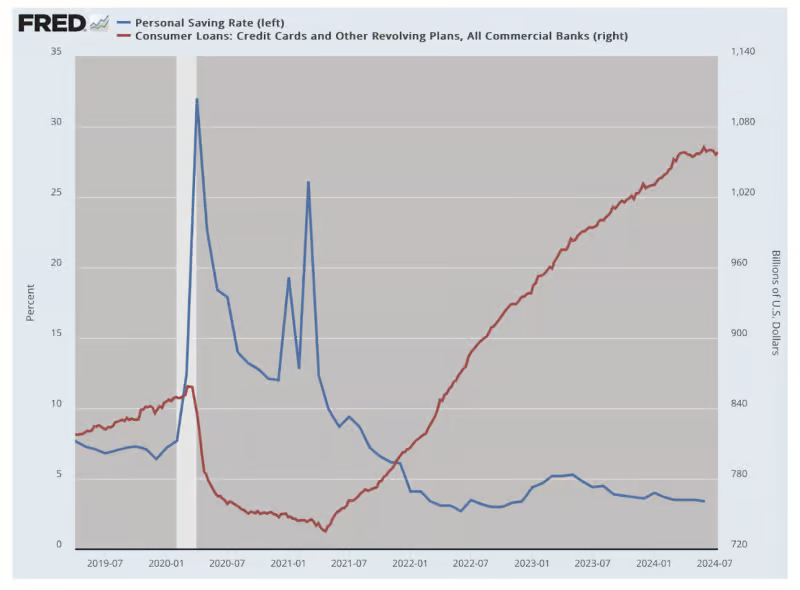

9. CBDCs are essential to the plan. A major ambition of the COVID response was the creation of a universal vaccine passport. It was deployed first in New York. The entire city was closed in all its public facilities to the unvaccinated. No one refusing the shot was permitted in restaurants, bars, libraries or theaters. Boston then replicated the plan, and so did New Orleans and Chicago. It faltered because business complained and also the software failed, despite the tens of millions spent. All these efforts were reversed but the plan itself revealed the larger agenda: control through data collection and enforcement. The ambition is not gone and will likely come back but a better and more comprehensive path is the central bank digital currency, now being deployed in many parts of the world. It allows universal surveillance, timed currency expirations and directed spending rationing to reflect political priorities. There is no question that the elites want this. 10. Financial markets will thrive until they do not. So far, in the course of the last crazy four years, we have been spared a serious financial crisis either in stocks or banks. This is not entirely unusual in the midst of a wild expansion of money and credit. After hitting prices and wages, the new money flows into financials, the rise of which is seen as fantastic news rather than simple price inflation. That said, the stock market is not the economy. It bodes well for people invested and stockpiling retirement accounts but does nothing for Main Street wage and salary earners. The lockdowns amounted to the world's largest and most elaborate economic head-fake in human history. It left the entire world less free and less prosperous, and with drained hopes that restoring normalcy can happen anytime soon. To add injury to the insult, most official institutions are manufacturing fake data to cover it all up. The post 10 Lingering Hangovers From Lockdowns appeared first on Daily Reckoning. |